[ad_1]

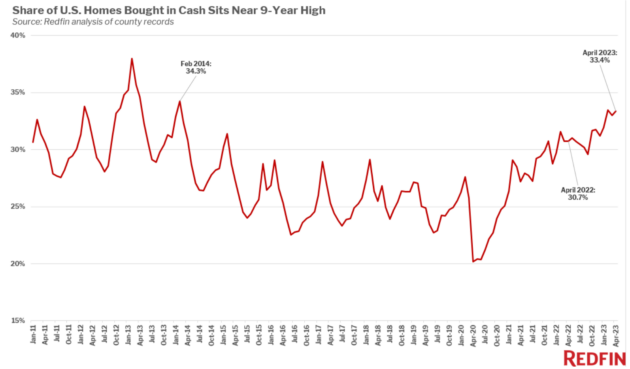

The share of U.S. homebuyers making all-cash purchases hit a decade-high in April, with one-third of buyers bypassing mortgage loan options, according to a Redfin report released Wednesday.

All-cash purchases accounted for 33% of home purchases in April, up from 30% a year earlier, Redfin found. In Seattle, 18.6% of homes were bought with all-cash offers, while the median down payment $141,000, the firm found.

Redfin analyzed county records across 40 of the most populous U.S. metros through 2011. It defines an all-cash purchase as a transaction without any mortgage loan information on the deed.

Redfin said all-cash purchasers are grabbing a larger chunk of homes because rates deter mortgage-dependent buyers more than all-cash buyers.

In early June, the 30-year fixed mortgage rate stood at 6.79%, approaching its highest level in 15 years.

Costlier mortgages discourage homeowners with fixed rates from selling their homes and prevents many would-be homebuyers from entering the market.

The typical U.S. homebuyer down payment was $52,500 in April, down 18% from a year prior, Redfin found. Down payments have been declining on a year-over-year basis since November due to three reasons, according to Redfin: “less competition among homebuyers, high mortgage rates and declining home prices.”

Redfin Senior Economist Sheharyar Bokhari said homebuyers who are in the position to make an all-cash offer face two choices: they can pay in cash to avoid hefty monthly interest payments, or get a loan and invest the extra cash in assets that return enough to offset the higher fees.

He added that homebuyers who cannot afford to make an all-cash offer have two choices: they can drop out of the housing market altogether, or accept the pricier mortgage rate.

In an already sluggish housing market, the rising trend toward cash payments could further weaken demand for startups selling mortgage products.

Seattle-based mortgage startup Tomo, which raised $110 million, laid off 44 employees last year as a result of higher interest rates. New York-based digital mortgage lender Better has also struggled.

Zillow Group’s mortgage business saw revenue decline 43% to $26 million in the first quarter.

[ad_2]

Source link